With the summer holidays fast approaching, many employers are considering hiring pupils or students to cover staff absences.

Although this practice is common and particularly flexible, it nevertheless remains subject to specific rules, which vary significantly depending on the type of contract used and the period of employment.

To this must be added an important legislative development, namely the extension of compulsory schooling to the age of 18 as from 1 September 2026, which is bound to alter certain recruitment practices.

In this context, it is essential to adopt the right reflexes in order to avoid the most frequent errors and to secure the employment of students.

Hiring students during school holidays

Luxembourg legislation allows employers to hire students during school holidays, subject to the conclusion of a specific contract: the student employment contract. This contract must comply with a number of conditions laid down in the Labour Code.

Who is eligible?

Students are defined as young people aged between 15 and 27 (up to the day of their 27th birthday), enrolled in full‑time education in Luxembourg or abroad. Anyone whose enrolment in school ended less than 4 months ago is also considered a pupil or student.

The student employment contract must be concluded in writing, at the latest at the time the student commences employment. A copy must also be sent to the Labour and Mines Inspectorate within seven days of the start of work. This notification may be made electronically via the MyGuichet.lu platform.

Where the student is enrolled in full-time education abroad, he or she may also be hired under a student employment contract during his or her own school holiday periods, even if these differ from those applicable in the Grand Duchy. In such cases, a certificate of enrolment serves to confirm the holiday period.

How long may you employ a student?

The total duration of employment of a student is strictly limited to two months per calendar year, across all employers and all contracts.

This cap corresponds to a maximum of 346 hours per year.

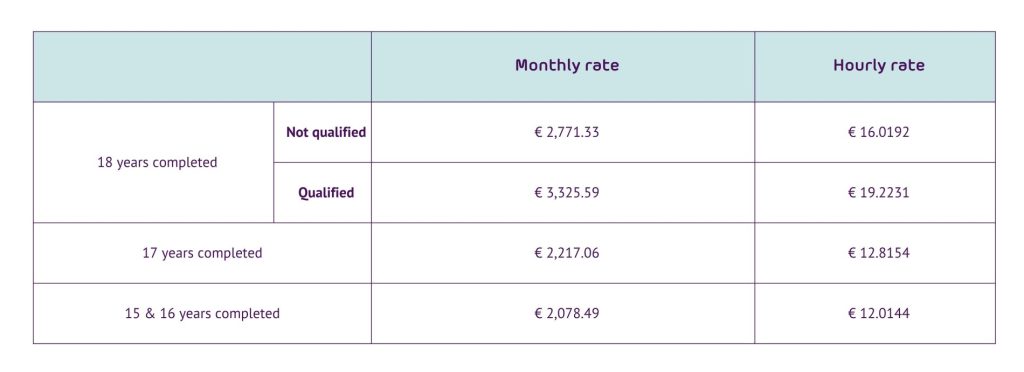

What remuneration must be provided?

The remuneration of pupils and students may not be lower than 80% of the social minimum wage, and varies according to age.

| % | Monthly gross salary (index 992.24) | Hourly gross salary (index 992.24) | |

| 18 and over, unskilled | 80% of 100% Statutory Minimum Wage | €2,217.06 | €12.8154 |

| 17 to 18 | 80% of 80% Statutory Minimum Wage | €1,773.65 | €10.2523 |

| 15 to16 | 80% of 75% Statutory Minimum Wage | €1,662.80 | €9.6115 |

What are the social security and tax obligations?

The student must be declared to the Centre Commun de la Sécurité Sociale (CCSS) [Joint Social Security Centre].

If the student does not have a national identification number (13-digit social security number), the employer must attach a copy of the student’s identity document to the affiliation request. For third‑country nationals, an application for a national identification number must be submitted to the Directorate General for Immigration.

No social security contributions are payable, except for the employer’s contribution to accident insurance which is paid by the employer.

Remuneration paid to students and pupils employed during school holidays is exempt from withholding tax, provided that the hourly gross wage does not exceed €18. However, this exemption is not automatic: the employer must submit a request to the Luxembourg Inland Revenue (Administration des contributions directes – ACD). Only one request per year is required; the certificate issued by the Luxembourg Inland Revenue then covers all students hired during the relevant year.

Leave, sickness, Sunday work: which rules apply?

Pupils or students employed during school holidays are not entitled to paid annual leave.

However, extraordinary leave granted for personal reasons (for example: birth, marriage, death of a family member, etc.) must be granted where the legal conditions are met, although no remuneration is owed by the employer during such absences.

In the event of illness, the student is likewise not entitled to continued payment of remuneration during the period of incapacity for work. Consequently, the employer is not required to declare this illness to the CCSS.

The rules regarding Sunday work and work on public holidays differ depending on the student’s age:

- Adult students may be employed on these days, subject to the application of the wage supplements provided for under ordinary law.

- Pupils and students aged 15 to 18 may also be employed on Sundays and public holidays, but under more restrictive conditions:

- Sunday work: a full compensatory rest day must be granted within the 12 days immediately following the Sunday worked plus a supplement of 100%;

- Work on a legal public holiday: a full compensatory rest day must be granted within the 12 days immediately following the public holiday worked plus remuneration at 300% of the normal hourly wage;

- In addition, pupils and students aged 15 to 18 must be exempt from work one Sunday out of two (with the exception of the hotel and restaurant sector during July and August, where this limitation does not apply).

Hiring pupils or students outside school holiday periods

When a pupil or student is not in a duly established school holiday period (in particular as evidenced by a certificate of enrolment), it is still possible to hire them under a specific fixed‑term contract, known as a “student fixed‑term contract.”

Who is eligible?

At present, compulsory schooling runs from age 4 to age 16, which in practice means that an employment contract can be concluded with a student as of the age of 16 outside school holiday periods.

However, this situation will soon change: under the Compulsory Schooling Act of 20 July 2023, compulsory education will be extended to the age of 18 as from 1 September 2026. As a result, except where legal exceptions apply, a pupil or student will need to have reached the age of 18 in order to be employed outside school holiday periods.

What about a student contract for a pupil under 18 that begins before 1 September 2026?

Article 16 of the Compulsory Schooling Act 20 July 2023 contains an important transitional provision: the extension of compulsory schooling to the age of 18 does not apply to pupils who already reached the age of 17 before 1 September 2026. In practice, it may be inferred from this provision that, in such cases, employment contracts already in force may continue to produce their effects beyond that date.

Furthermore, the law provides for a dispensation mechanism. A minor aged at least 16 who has signed an employment contract may be exempted from compulsory schooling for the duration of that contract, provided that a written request is submitted by the parents or guardians to the competent minister no later than eight days before the start of the dispensation. Such a mechanism could, in certain situations, allow an employment contract to continue beyond 1 September 2026, including for students who have not yet reached the age of 18.

What working time limits must be observed?

Weekly working time is limited to 15 hours on average, calculated over a period of one month or four weeks.

These contracts may be concluded successively with the same employer, for a maximum total duration of 60 months (5 years), including renewal(s). They may also be renewed more than twice, even where their total duration exceeds 24 months, without being reclassified as an open‑ended employment contract.

What remuneration must be provided?

The employer must pay at least a wage corresponding to the social minimum wage (currently €2,771.33 at index 992.24).

What are the social security and tax obligations?

Although they are pupils or students, those employed under a fixed‑term “student” contract outside school holidays are to be regarded as ordinary employees. They must therefore be affiliated to all Luxembourg social security schemes.

If the student does not yet have a national identification number (13-digit social security number), the employer must attach a copy of the student’s identity document to the affiliation request. For third‑country nationals, an application for a national identification number must be submitted to the Directorate General for Immigration.

From a tax perspective, the ordinary regime applies: the student is subject to withholding tax and is issued a tax card. In practice, however, where remuneration is limited to the statutory minimums, the student will generally not be taxed, since his or her income remains below the taxable threshold. The student may also benefit from tax credits (Crédit d’impôt pour salariés) (CIS) [Employee Tax Credit], Crédit d’impôt CO₂ salarié (CI-CO2) [Employee CO₂ Tax Credit], and Crédit d’impôt salaire social minimum (CISSM ) [Minimum‑Wage Tax Credit].

Leave, sickness, Sunday work: which rules apply?

Pupils and students employed under a fixed‑term “student” contract are entitled to statutory leave, calculated pro rata to their working time (maximum 15 hours per week). The same principle applies to legal public holidays.

As regards Sunday or public‑holiday work, there is no legal provision prohibiting adult pupils or students from being employed on such days; the ordinary wage supplements therefore apply where appropriate.

Conversely, pupils and students aged 16 to under 18 may not be employed on Sundays or legal public holidays, except in cases of force majeure or where the existence or safety of the undertaking so requires.

Finally, in the event of sickness, students are subject to the same regime as ordinary employees: they must notify the employer of their absence and provide a medical certificate. Periods of incapacity for work will be remunerated in accordance with the rules applicable to employees.

Conclusion

Hiring students offers employers a flexible solution, but requires a sound understanding of the applicable legal framework, which varies considerably depending on whether the activity takes place during or outside school holidays.

The entry into force of the extension of compulsory schooling to the age of 18 as of 1 September 2026 is therefore a major point of attention, likely to have a concrete impact on recruitment practices.

In this context, a prior analysis of the situations envisaged is essential to secure the use of the different types of contracts and to master their implications, particularly regarding working time, social security and taxation.

The legal team naturally remains at your disposal for any questions relating to these arrangements.