Here you will find all the latest news about HR management in Luxembourg!

1/ Contribution to the Chamber of Employees

2/ New developments for special contracts (CIE, CAE, CRE and professionalisation placements)

3/ Reminder of the rules for hiring pupils and students

4/ Final stretch for INFPC files

5/ Tax declaration forms available: Ready? Set, declare!

6/ What about the next indexation?

7/ Right to disconnect: beware of upcoming sanctions

8/ Pay transparency: Take action now!

9/ European Blue Card: increase in the salary threshold

1 – Contribution to the Chamber of Employees

As every year, employers are required to pay the contribution to the Chamber of Employees. This will be requested from employers via the account statement sent in July by the Joint Social Security Centre.

The contribution is set at €35 per employee and is deducted from employees’ net salary during the March payroll.

It should be noted that this contribution is payable only once per employee. In cases where an employee has multiple employers, the contribution for the Chamber of Employees is, in principle, payable by the employer for whom the employee works the greatest number of hours. If working hours are identical, which employer is responsible for collecting the contribution depends on the oldest affiliation.

In May, the Joint Social Security Centre will send all employers a statement listing the employees for whom they must pay the contribution, together with the corresponding amount.

2 – New developments for special contracts (CIE, CAE, CRE and professionalisation placements)

The Law of 3 March 2026, which shall enter into force on 1 July 2026, reforms the schemes for Contrats d’Initiation à l’Emploi (CIE) [Employment Initiation Contracts], Contrats d’Appui-Emploi (CAE) [Employment Support Contracts] and Contrats de Réinsertion-Emploi (CRE) [Employment Reintegration Contracts] and the Stage de Professionnalisation (SP) [Professionalisation training intership]. The aim is to strengthen professional integration, particularly for young people.

The compensation schemes for CIE and CAE are now aligned with that of the CRE. From now on, the Agence pour le Développement de l’Emploi (ADEM) [National Employment Agency] will pay the allowance directly to the beneficiary, while the employer’s financial contribution is simplified.

Regarding leave, the reform ends the differentiated rules that previously applied. Beneficiaries of a CIE, CAE or CRE are now all subject to the company’s recreational leave regime, prorated to the duration of their contract.

Furthermore, access to the professionalisation placement is also broadened: it is now open to all jobseekers registered with ADEM, regardless of age. Its link with the CIE is strengthened to facilitate pre‑employment pathways. Limited to 6 weeks (or 9 weeks for highly qualified profiles), this placement enables employers to assess a candidate in real working conditions without resorting to a longer scheme immediately.

All these changes form part of a broader effort to simplify administrative procedures and to secure professional integration pathways for employers and beneficiaries alike.

3 – Reminder of the rules for hiring pupils and students

With the summer holidays approaching, some of you may already be considering hiring pupils or students to cover staff absences. Certain formalities are in force to that end.

The contract between the employer and the student must be concluded in writing, at the latest on the day the student starts work.

The student contract must be drawn up in three original counterparts:

- one for the student;

- one for the employer;

- one for the Inspection du travail et des Mines (ITM) [Labour and Mines Inspectorate]: the contract and a copy of the identity card must be sent to the ITM within 7 days of the start of the contract, either by ordinary post or via MyGuichet.lu.

The period of employment may not exceed 2 months or 346 hours per calendar year, regardless of whether the work is performed under one or several contracts, and regardless of the number of employers. It is therefore possible to conclude one or more part‑time student contracts over a period exceeding two months during one or more school holidays, provided that the total does not exceed 2 × 173 hours = 346 hours per calendar year.

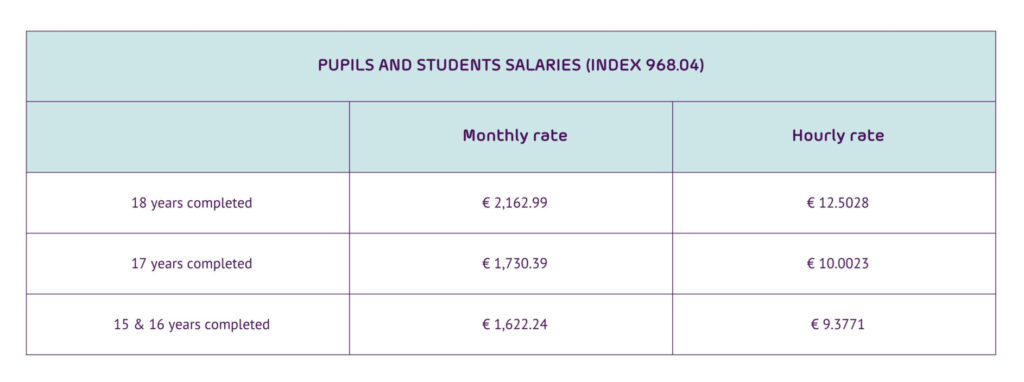

For its part, the remuneration paid to a pupil or student may not be lower than 80% of the social minimum wage. At index 968.04, the pupil/student is entitled to the minimum amounts shown in the table below, adjusted according to age.

The employer is required to submit a declaration of entry to the Joint Social Security Centre. However, only the employer’s contribution for accident insurance is payable.

Furthermore, the student is exempt from income tax provided that their hourly wage does not exceed €18/hour. The student’s gross salary will therefore be identical to their net salary. To benefit from this exemption, the employer must submit a request to the Luxembourg Tax Authorities (ACD). This request must be made once per year for all students; it is therefore not nominative. Employers are advised to submit this request when hiring the first student of the calendar year.

4 – Final stretch for the INFPC files

As you know, every year employers may benefit from financial aid relating to training costs invested during the previous year. To do so, it is essential to submit your Institut National pour le Développement de la Formation Professionelle Continue (INFPC) [National Institute for the Development of Continuing Vocational Training] file before 31 May.

Employers may receive financial aid amounting to 15% of the cost invested in 2025 in the training of their employees.

The main costs eligible for reimbursement are:

- Salaries of participants and internal trainers;

- Fees of external training providers;

- Travel, accommodation and meal expenses linked to training.

Training investment is capped according to company size:

- 20% of payroll for companies with 1 to 9 employees;

- 3% of payroll for companies with 10 to 249 employees;

- 2% of payroll for companies with more than 249 employees.

Thus, for a company with 5 employees, reimbursement may reach 15% of the 20% of payroll invested in training; for a company with 100 employees, reimbursement may reach 15% of the 3% of payroll invested.

The aid is increased by 20% for employees trained while having no diploma and less than 10 years’ seniority, or if they are over 45 years old.

To obtain this reimbursement, a specific file must be completed and documented, including invoices, signed attendance lists, employee data and payroll information. This co‑funding request to the National Institute for the Development of Continuing Vocational Training (INFPC) must be submitted no later than 31 May 2026.

5 – Tax declaration forms available: Ready? Set, declare!

The tax declaration forms for 2025 income have been available since 7 April 2026. The income tax return for individuals for the 2025 tax year must be duly completed, signed and submitted no later than 31 December 2026.

Three filing channels are now available:

- Via the electronic assistant on MyGuichet.lu, requiring LuxTrust access;

- Via paper form, available on the website of the Administration des Contributions Directes (ACD) [Luxembourg Inland Revenue], to be sent by post to the competent tax office;

- Via PDF form, available on the ACD website, to be submitted electronically to the competent tax office

6 – What about the next indexation?

The last indexation took place on 1 May 2025.

An automatic indexation is triggered whenever the six‑month average of the index shows a 2.5% difference compared with the last reference value.

Based on the current inflation rate and STATEC estimates, the next indexation could occur in May or June 2026, although this cannot be confirmed at this stage. The upcoming STATEC publication will confirm this — or not.

By way of reminder, indexation is mandatory and applies to all employees under a Luxembourg employment contract, as well as students, trainees and apprentices, whose remuneration will increase by 2.5%.

7 – Right to disconnect: beware of upcoming sanctions

Although the obligation to implement a right‑to‑disconnect framework has been in force since 2023, administrative sanctions will apply only as of 1 July 2026.

Since 4 July 2023, Luxembourg has had a legal framework regulating employees’ right to disconnect. These provisions require employers to implement an appropriate system governing the use of digital tools for professional purposes, through a charter, internal regulation or equivalent document.

Implementation of the right‑to‑disconnect scheme:

- By collective agreement or subordinate agreement;

- At company level, in compliance with the powers of the staff delegation, where one exists, to wit:

- in a company with fewer than 150 employees at the last elections: the staff delegation must be informed and consulted;

- in a company with at least 150 employees at the last elections: the staff delegation has a co‑decision right;

- In the absence of a staff delegation, by unilateral decision of the employer after informing employees.

If no compliant right‑to‑disconnect scheme is implemented, the employer may face an administrative fine ranging from €251 to €25,000, imposed by the ITM. However, these sanctions will only apply as of 1 July 2026.

8 – Pay transparency: Take action now!

In May 2023, the European Union adopted Directive (EU) 2023/970, which aims to strengthen equal pay between women and men by introducing extended obligations regarding pay transparency. To date, Luxembourg has not yet adopted the national law that will implement this directive; however, the directive already establishes a general framework.

The purpose of the directive is to strengthen equal pay between women and men by ensuring that remuneration policies are objective, documented and transparent.

In practical terms, companies will be required to communicate pay levels or pay ranges from the recruitment stage, prohibit any request relating to a candidate’s salary history, and allow employees to access the criteria used to determine their pay and their career progression.

In the medium term, employers reaching certain workforce thresholds will also be subject to publication and reporting obligations regarding pay gaps. In the event of litigation, the burden of proof may be reversed, placing the onus on the employer.

This reform requires a thorough review of remuneration practices and encourages employers to begin preparing at an early stage. For reminder, Member States have until 6 June 2026 to transpose the directive.

To learn more about employers’ new obligations, you can read our dedicated article via the link below :

Salary transparency: a forthcoming obligation for employers in Luxembourg

9 – European Blue Card: increase in the salary threshold

The salary threshold required for obtaining a European Blue Card in Luxembourg has been raised since March 2026.

Third‑country nationals (i.e., non‑EU and non‑EEA nationals) with high qualifications may access the Luxembourg labour market through this specific residence permit: the European Blue Card.

To qualify, several conditions must be met: First, the highly qualified worker must receive a gross annual salary exceeding the minimum threshold, set at €65,652 as of 3 March 2026, compared with €63,408 on 18 March 2025. This threshold is a key eligibility criterion for the Blue Card.

Beyond remuneration, the third‑country national must have an employment contract of at least six months. They must also demonstrate the high professional qualifications required for the position concerned: either by meeting the requirements applicable to the non‑regulated profession in question, or by fulfilling the conditions applicable to a regulated profession, as specified in the employment contract.

Would you like to receive the latest news concerning HR in Luxembourg directly in your inbox? Sign up for My HR Update: https://www.securex.lu/en/#legal-updates