Here you will find all the latest news about HR management in Luxembourg!

1/ Tripartite agreement: what consequences for employee payroll?

2/ New social parameters as of 1 June 2026

3/ New tax regime forthcoming for stock options

4/ Beware of fraudulent medical incapacity certificates

6/ Apprenticeship contracts: signing season is open

1/ Tripartite agreement: what consequences for employee payroll?

Following the tripartite agreement of 8 June 2026, concluded between the Luxembourg Government and the social partners, a bill has been submitted to the Chamber of Deputies with the aim of supporting employees’ purchasing power. Below are the main measures that will directly affect salary calculations.

Introduction of a crédit d’impôt conjoncture (CIC) [Cyclical Tax Credit]

To bolster purchasing power and curb inflation, the Government has decided to reintroduce temporarily as in 2023, a cyclical tax credit (CIC) for the period from 1 June 2026 to 31 December 2026. This tax credit is intended to offset the postponement of the adjustment of the tax scale following the indexation that took place on 1 June 2026 to 1 January 2027.

The CIC will be paid directly to the employee through payroll, in the same way as the crédit d’impôt salaire (CIS) [salary tax credit] and the credit d’impôt salaire social minimum (CISSM) [minimum social wage tax credit]. Its cost will be borne entirely by inland revenue. The amount varies according to the employee’s monthly gross salary.

| Monthly gross salary | CIC amount |

|---|---|

| € 1,125 to € 1,250 | Between € 0 and € 2 per month |

| € 1,250 to € 2,100 | Between € 2 and € 3.50 per month |

| € 2,100 to € 4,600 | Between € 3.50 and € 22 per month |

| € 4,600 to € 9,500 | € 22 per month |

| € 9,500 to € 9,925 | Between € 22 and € 24 per month |

| € 9,925 to € 14,175 | € 24 per month |

| € 14,175 to € 14,916 | Between € 24 and € 27.13 per month |

| above € 14,916 | € 27.13 per month. |

Increase of the salaire social minimum (SSM) [minimum social wage] and the CISSM as of 1 January 2027

Introduced in 2019, the CISSM is a support mechanism for employees with the lowest incomes. Under the new tripartite agreement, it has been decided to improve progressively the purchasing power of employees earning a low wage or one close to the SSM through several measures:

- a structural increase of the SSM of around 3.8% from 1 January 2027;

- an increase in the CISSM, which will rise from €81 to €179 from 1 January 2027;

| As of 1 January 2027 | CISSM amount |

|---|---|

| Monthly gross salary between € 1,800 and € 3,000 | € 179 per year |

| Monthly gross salary between € 3,000 and € 3,600 | Decreasing amount from € 179 to € 0 per year |

- a further increase in the CISSM, which will rise from €179 to €200 as of 1 July 2027;

| As of 1 July 2027 | CISSM amount |

|---|---|

| Monthly gross salary between € 1,800 and € 3,000 | € 200 per year |

| Monthly gross salary between € 3,000 and € 3,600 | Decreasing amount from € 200 to € 0 per year |

According to the explanatory memorandum, these measures should increase the purchasing power of beneficiaries of the unskilled SSM by around € 200 net compared with the situation in June 2026. Thanks to the strengthening of the CISSM, taxation for taxpayers in tax class 1 earning the unskilled SSM should also be neutralised.

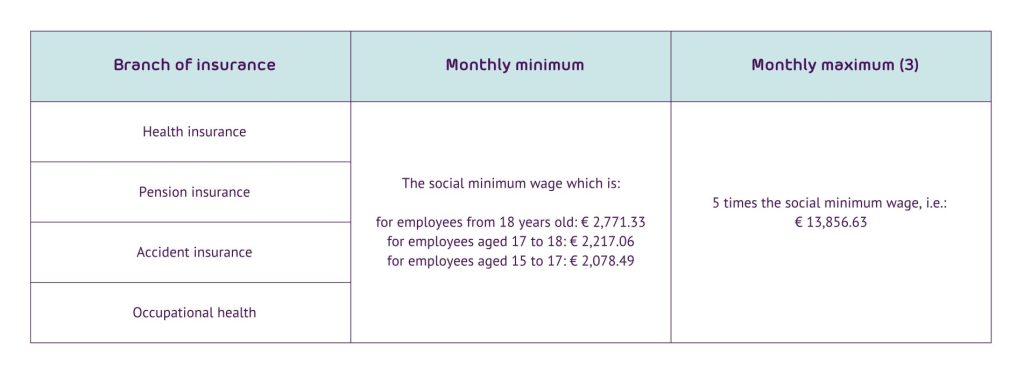

2/ New social parameters

A new index bracket (992.24) has been in force since 1 June. This results in new social parameters applicable as of 1 June 2026.

Minimum and maximum contributory bases

(3) For 2026, the annual maximum for the various insurance branches amounts to € 164,589.81. This maximum does not apply to long‑term care insurance. However, the assessment base for long‑term care insurance is reduced by one quarter of the unskilled minimum social wage, i.e. € 692.83.

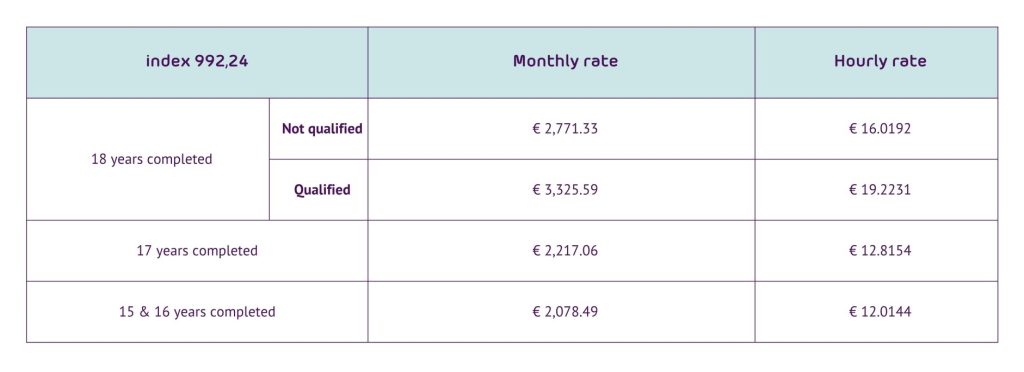

Minimum social wage

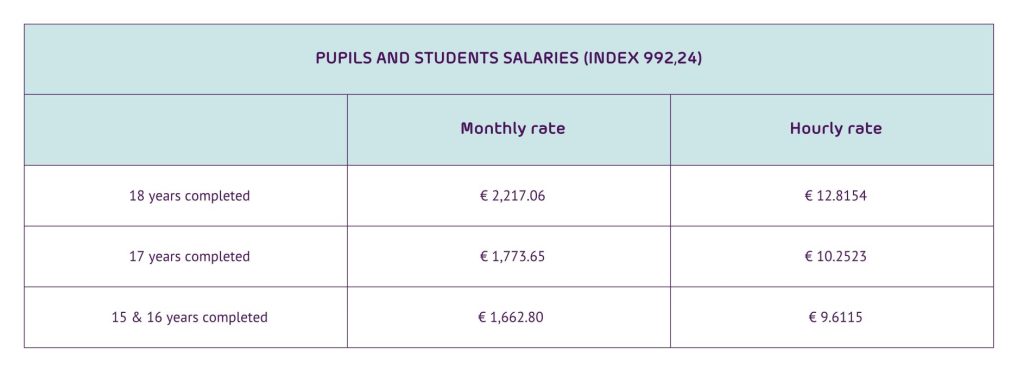

Remuneration of pupils and students employed during school holidays

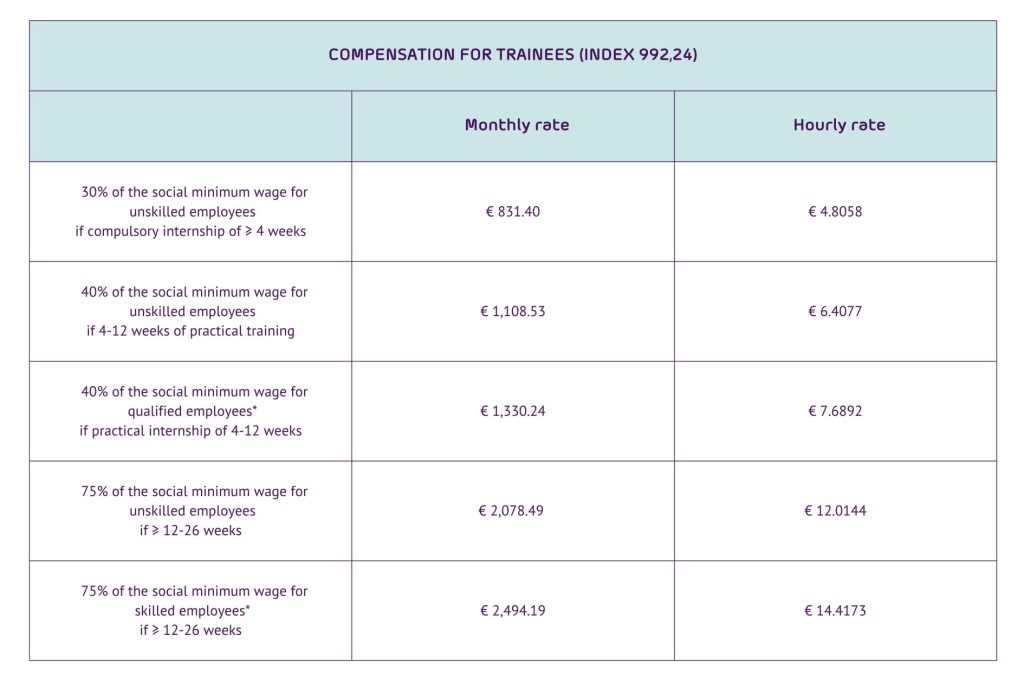

Remuneration of trainees

*For trainees who have successfully completed the first cycle of higher or university education (BTS or Licence/Bachelor), the reference salary is the minimum social wage for skilled workers as provided for in Article L .152 8 of the Labour Code.

3/ New tax regime forthcoming for stock options

Bill No. 8782 was submitted on 1 July 2026 to strengthen the appeal of Luxembourg’s ecosystem for young innovative companies. The aim is to support their development in Luxembourg by offering new tools to attract and retain highly qualified talent.

The bill also seeks to clarify and enshrine in law the general tax regime applicable to option plans granted to employees.

New regime dedicated to young innovative companies

Subject to meeting certain conditions, young innovative companies will be able to introduce share option plans that will benefit from a favourable tax regime for their employees. These companies must in particular:

- have been incorporated for less than 10 years;

- employ fewer than 150 full‑time equivalent (FTE) employees;

- have a balance sheet total or turnover not exceeding €30 million;

- carry out an innovative activity, with:

- at least two persons working full‑time;

- research and development expenditure representing at least 15% of operating expenses.

The main advantage of this new regime lies in the tax treatment of options that are not freely negotiable (i.e. options that are neither listed on a stock exchange nor freely transferable).

Unlike the regime currently in force, no taxation would be due at the time of grant or exercise of the options. The employee would only be taxed upon the sale of the acquired shares, at a particularly favourable rate corresponding to one quarter of the overall tax rate. This regime would apply to options granted from 2027 onwards.

Clarification of the general regime applicable to option plans

The bill is not limited to young innovative companies. It also clarifies the general tax regime applicable to option plans granted by companies that do not meet the conditions of the new regime or have chosen not to apply it. In order to improve legal certainty and the readability of the rules, existing principles will henceforth be incorporated directly into Luxembourg tax law.

The applicable regime will depend on the nature of the options granted. Freely negotiable options will be taxed upon their attribution, whereas options that are not freely negotiable will be taxed only upon their exercise. Where the acquired shares are subject to a lock‑up period, a flat‑rate discount of 5% per year of lock‑up may be applied, up to a maximum of 20%.

Finally, under both the new regime and the general regime, the employer must complete the required reporting formalities with the tax administration before 1 March of the year following the grant or exercise of the options, as applicable.

4/ Beware of fraudulent medical incapacity certificates

In response to the increasing number of irregular medical certificates, the Caisse nationale de santé (CNS) [National Health Fund] is warning employers and now refuses all certificates obtained via online platforms without consultation or medical examination, as well as those issued by doctors considered “unknown”.

To assist insured persons and employers in identifying the certificates concerned, the CNS publishes on its website a list of doctors whose incapacity certificates are refused. This list is updated regularly and can be consulted directly on the CNS website.

When a certificate is declared invalid by the CNS, no benefit will be paid for the period of incapacity concerned. The employer will be informed. If the employee is still within the period during which salary is maintained at the employer’s expense, the employer will not be able to obtain reimbursement of the corresponding wages and may, where appropriate, reclassify the absence as unjustified and adjust the employee’s pay accordingly. If the employee is already under the responsibility of the CNS, no sickness benefit will be paid for the period covered by the certificate.

Regardless of any consequences under employment law, an insured person who uses such certificates is liable to administrative fines and possible legal proceedings initiated by the CNS.

The amount of the fine depends on the duration of the “false certificate”:

- Incapacity lasting three days or less: € 200

- Incapacity lasting more than three days: € 500

- In the event of a repeat offence, regardless of duration: € 750

5/ Summer will be hot!

During this period of extreme heat, the Labour and Mines Inspectorate recently issued a press release with recommendations and good practices in the event of high temperatures.

By way of reminder, the employer is required to ensure the health and safety of employees in the workplace. In periods of heatwave, the employer must therefore implement measures both for work carried out outdoors and within work premises.

For outdoor work, the employer must provide well‑ventilated shaded areas, supply workers at their workstations with drinking water, reduce tasks requiring sustained and prolonged physical effort, and provide mechanical assistance for strenuous work.

Within work premises, the employer must monitor temperatures and thermally insulate existing buildings and rooms, and provide employees with means to combat heat, such as fans or air‑conditioning units. The employer must also make drinking water available, in sufficient quantity, for all employees of the company.

6/ Apprenticeship contracts: signing season is open

Apprenticeship is a form of vocational training that includes periods of school‑based learning as well as periods of practical training in a professional environment.

It prepares learners for the attainment of various qualifications and exists in two forms:

- Initial apprenticeship, which concerns minors aged at least 15;

- Adult apprenticeship, which concerns adults and enables them to complete, supplement, or acquire vocational training through the alternating apprenticeship system.

To hire individuals under this type of contract, as of March employers were required to submit apprenticeship post declarations to ADEM’s vocational guidance service.

Apprenticeship contracts must be concluded from 16 July to 1 November.

Would you like to receive the latest news concerning HR in Luxembourg directly in your inbox? Sign up for My HR Update: https://www.securex.lu/en/#legal-updates